Have you ever had this moment: at 2 AM, the kids are finally asleep, you switch off the lamp, and your phone pings with this month’s mortgage debit. You take a deep breath and quickly calculate: after the salary clears the loan, the kids’ tutoring, the groceries, the parking fee — this month is another wash. Then you scroll past a news headline: “Central bank holds benchmark rate steady, 10-year Treasury yield dips slightly.”

You stare at the words. You know each one, but together they read like a foreign language. You think: how does this affect me? Will it lower my mortgage? You swipe away. What you don’t know is that this thing you don’t understand is squeezing your mortgage rate, your next paycheck, and even the meager returns in your stock account.

It’s the elephant in the room. It affects you every day, but you’ve never really looked at it. That invisible giant is the bond market — and its size dwarfs the stock market. You watch stock tickers all day, but compared to bonds, those moves are tiny ripples. Most people have no idea it exists.

Don’t worry. Today I won’t use any jargon. Let’s just sit at the convenience store and have a coffee. In 15 minutes, I’ll completely strip down this thing that’s been hijacking your life.

What Exactly Is a Bond? Just a Polite IOU

You say: what’s the best way for ordinary people to understand something? Use a real-life analogy.

Imagine your less-reliable younger brother comes running to you: “Bro (or sis), I found a bubble tea franchise and I’m short NT$200,000. Lend it to me. Next year I’ll pay you back NT$200,000 plus an extra NT$10,000 in interest.” Will you lend it?

Don’t answer yet. You’ll definitely ask: “Why should I?” Because if you had that NT$200,000 yourself, you could put it in a time deposit or some safe product and earn a few thousand in interest. If you give it to him, you lose that opportunity — this is called opportunity cost. You gave up your chance to earn, so he has to compensate you. That NT$10,000 is the compensation.

OK, business is business even with family. You make him write an IOU: “Brother X borrowed NT$200,000 from sister Y today, agrees to repay NT$200,000 principal plus NT$10,000 interest one year from today.” This piece of paper is a bond. That’s how simple it is.

A bond is a formal IOU with a name on it. It clearly states: who borrowed, how much, when they’ll pay it back, and what the interest is. Individuals borrow, but companies and governments borrow even more. A company wants to expand, build a new factory, hire people, but doesn’t have enough cash — so it borrows from the market. The paper it writes is a corporate bond. The government needs to build roads, hospitals, and fund the military, but can’t collect enough tax revenue right away — so it borrows from the market. The government’s paper is a government bond (or “Treasury bond” at the national level).

So you see, bonds aren’t fancy at all. They’re the most basic borrowing-and-repaying contract we have.

Why Do the Rich Obsessively Buy Bonds? Two Words: Safety

If it’s just an IOU, why don’t the rich put all their money into stocks to double it? Why are they obsessed with bonds?

The answer is simple: two words — safety.

Think about it. If you lend money to your brother, what’s your biggest fear? That his business fails and he runs off, taking your NT$200,000 principal with him — that’s credit risk. But what if you lend the money to your local government, or to the country itself? You might say governments can go bankrupt too — theoretically yes, but the probability is tiny. When a country defaults, the consequences are enormous.

So a stable country’s government bonds are considered among the safest assets in the world.

What matters most to the rich isn’t making the most — it’s staying alive. They can’t park tens or hundreds of billions in a stock-market roller coaster — 10% up one day, 20% down the next. Their core strategy is: use most of the money to buy a pile of stable income-generating assets like government bonds as ballast, and use only a small portion for high-risk, high-return bets.

This is asset allocation: you’re not trying to make the most money, you’re trying to make the steadiest money. We ordinary folks keep dreaming of betting a bicycle into a motorcycle. The truly rich are worried about a fumble turning a motorcycle into a bicycle.

Banks, insurance companies, pension funds — these giant institutions all think the same way. They have to pay deposit interest, insurance claims, and pensions every day. They can’t afford to lose. For them, bonds are the lifeline.

Four Key Terms: Principal, Coupon Rate, Maturity, Yield

I know you tune out the moment you hear “coupon rate” or “yield to maturity.” Let’s keep using the brother example.

One: Principal (face value). The NT$200,000 you lend your brother is the principal. On a bond, this is called the face value. The most basic piece.

Two: Coupon rate. This is the interest rate you agreed on, in writing. If you agreed on 5%, then it’s 5%. Your NT$200,000 earns you NT$10,000 in interest per year. This is the coupon rate.

A small etymology: in the old days, bonds were literally printed pieces of paper with small detachable coupons along one edge. On each interest-payment date, you’d tear off a coupon and redeem it for cash. The word “coupon” stuck around — that’s why people still call receiving interest “clipping the coupon,” even though everything is electronic now.

Three: Maturity. When your brother said “one year,” that one year is the maturity date. Could be 3, 5, or 10 years. The longer the time, the higher the uncertainty, so usually the higher the interest.

Four: Yield. This is the part that confuses everyone. Listen carefully — the coupon rate is fixed at issuance. The yield is the actual return you make if you buy the bond today at its current market price.

Why the difference? Because bond prices change.

Suppose the day after lending the money, you need cash urgently. You take the IOU to your neighbor Old Wang: “Old Wang, my brother owes me NT$200,000, due in one year, paying 5% interest. I’ll sell it to you for NT$195,000 — want it?” Old Wang does the math: his cost is NT$195,000, in one year he gets NT$200,000 principal plus NT$10,000 interest, total NT$210,000. He made NT$15,000. His actual return isn’t 5%, it’s about 7.7%. That 7.7% is the yield.

Get it? The lower the bond’s price, the higher your yield when you buy it. Conversely, if the IOU is hot — everyone thinks your brother is reliable and the bubble tea shop will thrive — and someone offers NT$205,000 for it, your effective cost goes up, your profit shrinks, and the yield drops.

Here’s the key insight — the most counter-intuitive seesaw of the bond market: when interest rates go up, bond prices go down. When interest rates go down, bond prices go up.

Remember the news about the US “aggressive rate hikes” and “global bond market crash” a couple of years back? Now you understand: the central bank pushed benchmark rates up, so newly issued bonds pay more interest — say from 3% to 5%. That makes your old 3% bond less attractive, so you have to discount it to sell, and the price crashes.

Grasp this one point, and you understand half of the bond market. Next time you see a headline about “bond yields soaring,” your brain should immediately think: oh, that means bond prices are plunging.

The Central Bank, Yields, and Inversion: How Does It Affect You?

Who decides the interest rate? It’s not just people shouting. There’s one institution that controls the master faucet of all money in the economy — the central bank (the Federal Reserve in the US, the People’s Bank of China in mainland China, the CBC in Taiwan).

The central bank sets a base rate, like the rediscount rate. Think of it as the water level in a giant water tower. When the water level rises, every faucet connected to it gets higher pressure. Banks borrowing from the central bank pay more, so the deposit rates they offer you and the loan rates they charge companies both go up. When the level falls, every faucet’s pressure drops and borrowing gets cheaper.

The central bank raises or lowers this water level to step on the brake or press the gas pedal of the economy.

But note: the central bank only sets a benchmark. The actual rate that gets traded in the market is the market rate — for example, the 10-year Treasury yield we hear about constantly. That yield is the cumulative bet of all the smartest money in the market on what the next ten years of growth, inflation, and central bank policy will look like. It moves every day.

If the market thinks the economy will heat up and inflation will rise, traders expect rate hikes, and bond yields climb in advance. If the market thinks the economy is cooling toward recession, traders expect rate cuts, and yields fall in advance.

So watching the 10-year Treasury yield is like peeking at the weather forecast of the smartest, biggest-pocketed players in the market.

Three Direct Ways It Affects You

First, your mortgage. When you borrow from a bank, how do they set the rate? They say: “Our base rate plus 1.5 percentage points.” Their base rate is heavily influenced by the market Treasury yield, especially the 10-year. The bank is a business. It has two choices: A) Lend to you, where there’s real risk — if you default, the bank has to seize and auction your home, which is a hassle; B) Buy 10-year government bonds, rock-solid, lower yield but absolutely safe. If the Treasury yield is 3% and your mortgage rate is only 3.5%, the bank thinks the extra 0.5% isn’t worth the default risk.

So when Treasury yields rise, the bank’s cost of capital rises, your mortgage rate almost certainly follows, and those extra few hundred or thousand dollars a month come straight from this.

Second, your job. Does your company need to borrow to grow? If bond yields are low, borrowing is cheap, and companies dare to expand and hire. If yields are high, borrowing is expensive, and the first thing companies do is cut headcount, freeze hiring, and slash budgets. Your annual raise — and even your job security — are tied to this invisible water tower.

Third, your stocks. This is the most subtle link. Suppose government bonds are yielding 5% risk-free. You don’t have to do anything — just lend to the country and pocket 5%, no stress, no brain work. Stocks might only return 7% per year, with real risk of bankruptcy and 50% drawdowns. What would you choose? Smart money doesn’t take 50% downside risk for an extra 2%. So traders sell stocks and buy bonds, and the more sellers, the lower the price.

Conversely, if Treasury yields are only 1% — barely beating inflation — people feel like bonds are a slow death. Money flows from bonds to stocks hunting higher returns, and the stock market finds support.

That’s why rate cuts usually help stocks rise, and rate hikes make stocks shiver.

Yield Curve Inversion: The Yellow Light Before Recession

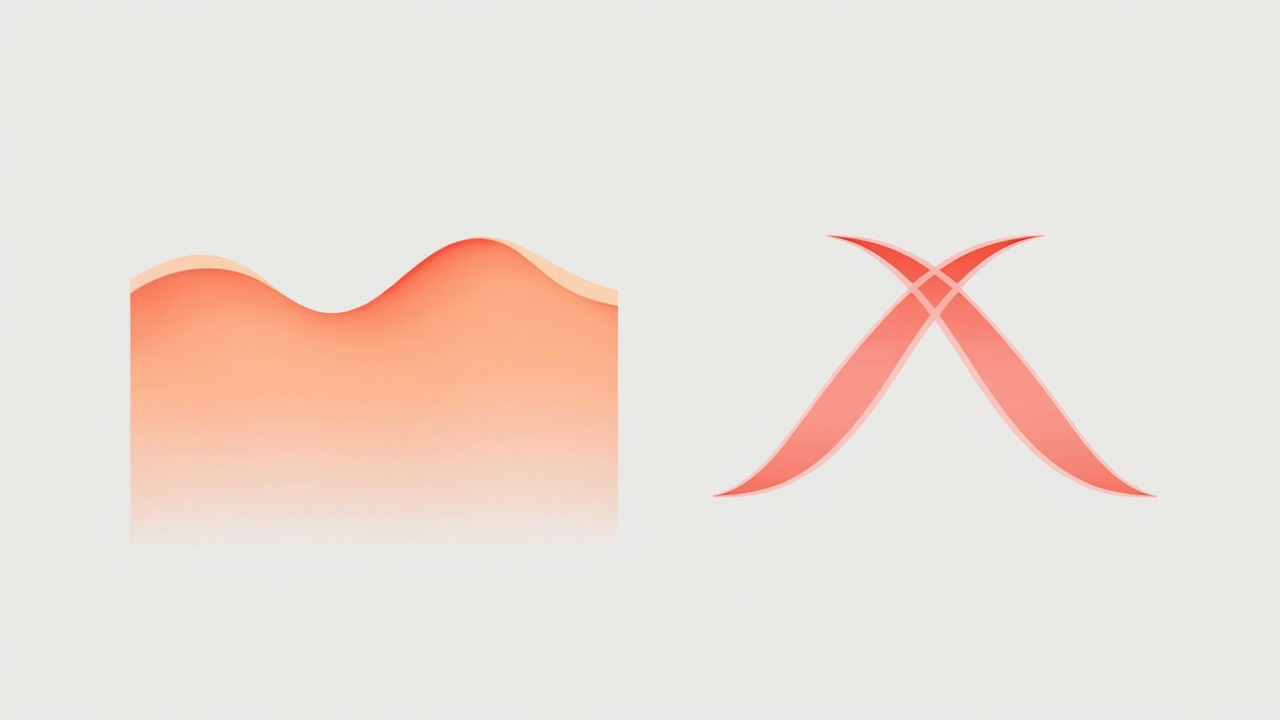

Now you can already beat 90% of ordinary people. Let’s take one more step — get familiar with a term that always appears in recession news: the yield curve inversion.

It’s not complicated. When you go to the bank, 1-year deposits pay 1.5%, 3-year pay 2%, 10-year pay 2.5% — that’s normal. The longer the term, the higher the uncertainty, the higher the reward. Connecting these rates, you get a curve that slopes upward — the normal curve.

But occasionally a strange phenomenon appears: 1-year rates are higher than 10-year rates. Say 1-year deposits pay 5%, 10-year only 3% — that violates intuition. Why is short-term more expensive than long-term?

It means investors are extremely pessimistic about the future economy. They think: the high rates now are temporary because the economy is about to fail, and the central bank will have to slash rates aggressively to save it. After rate cuts, all rates will fall, including long-term bond rates. So they rush to buy long-term bonds now to lock in the high rates. The buying pushes long-term bond prices up, and as prices rise, the actual yield (what you really earn) falls. Eventually long-term yields drop below short-term yields. This is the yield curve inversion.

Why is this signal so scary? Because over the past decades, almost every US recession has been preceded by this phenomenon. It’s like a yellow warning light telling every driver: danger ahead, prepare to brake. It doesn’t mean you’ll lose your job tomorrow, but it’s an extremely strong, real-money expression of worry from the market.

The 3-Bucket System: An Action Plan You Can Start Tonight

After all this macro talk, you might feel even more anxious. So many things control my life — what do I do? I can’t control the central bank.

Right, you can’t control the central bank or the market rate. But you can change one thing: the way you think about risk and return.

The biggest problem for ordinary people isn’t having too little money. It’s chasing returns and ignoring risk. You see others make money in stocks, you can’t sit still, you pour all your savings in hoping to double up, and the moment it drops you can’t sleep, you curse and cut your losses.

Every dollar you have has a mission: your kid’s tuition, next year’s travel fund, retirement twenty years from now. You can’t gamble tomorrow’s limit-up with the retirement money you won’t touch for twenty years.

This is the most basic and most important lesson from the bond market: your asset allocation must include a ballast — it doesn’t exist to make you rich, it exists to give you stability, to let you sleep at night.

What can this safety net be? For the rich, it’s government bonds. For you and me, it might be a pile of emergency savings in a time deposit, a comprehensive insurance policy, or even a 12-month living expense cushion in an account you never touch. This money isn’t for making money. Its only goal is to make sure no matter how rough the world gets outside, your life inside isn’t flipped over.

Some people bet their entire net worth in a casino. Some people risk only 10% of their spare cash and keep the other 90% in a moat. Ten years later, the first group might be rich or might be broke. The second group will still be sitting at the table, alive and stable. In the end, investing isn’t about who makes the most. It’s about who lasts the longest. Life is the same.

So I don’t recommend you open a bond account tomorrow or start studying the yield curve — that’s not relevant to where you are now. The only action I want you to take tonight is this:

Open your budgeting app tonight, or grab a piece of paper, and split your money into three buckets.

Bucket One: Survival

This money absolutely cannot be touched. Keep it in a demand account, time deposit, or ultra-safe money-market fund. This is your ballast when the sky falls. The amount is 3 to 6 months of living expenses. Until this is fully funded, don’t even think about investing.

Bucket Two: Stability

This money is for things 3 to 5 years out — a new car, renovations, your kid’s college tuition. You can put it in ultra-low-risk products or something like a bond fund with low volatility. The point is capital preservation, not getting rich.

Bucket Three: Betting

This is the money you can fully afford to lose. Use it to learn something you’re interested in, take a course to upgrade your skills, try a small side hustle, or buy that stock or fund you’ve been eyeing. Best case, you make money. Worst case, you can take it.

That’s it. Three steps. Pick up a pen and start sorting now. Don’t try to change everything at once. Pick one to start with — even if it’s just moving 10% of this month’s salary from “spend freely” to “survival bucket,” you’ve already started.

Closing: Your Future Self Will Thank You for Starting Today

Let’s end with a ten-year perspective.

If you continue to ignore risk, pinning all your hopes on “tomorrow will be better” or “some guru will make me rich,” ten years from now — at 45 or 55 — you’ll have hit the career ceiling, your parents will be aging and ailing, your kid will be heading to college with expenses everywhere, and when you open your account, you won’t find anything called “nest egg.” Just a paycheck that disappears by month’s end. That fear of the future, that elephant in the room, will finally be sitting on your chest.

But if you start today — even one tiny thing, even just splitting your money into buckets — ten years from now, you’ll be surprised. That survival bucket will quietly hold a heart-easing pile of cash. That stability bucket will be enough to cover tuition and a family trip without panic. You won’t fear layoffs because you have the底气 (backing) to say no. You won’t lose sleep over short-term market swings because you know that’s just a game inside your betting bucket.

Real freedom isn’t about how many choices you have. It’s about having the底气 to choose not to do something.

Start by understanding this IOU. Start by splitting your buckets tonight. Reality is hard, but it’s OK — I’m here with you, softening it bit by bit.

Disclaimer: This article is for educational and informational purposes only and does not constitute investment advice. Investing involves risk, and past performance does not guarantee future returns. Please assess your own risk tolerance carefully before making any decisions.

Image Generation Prompts

Image 1: The Elephant in the Room

- Placement: Article opening hero banner

- Emotional Anchor: Metaphor, oppression, awakening

- Color Tone: Dark grey + a hint of cold light

- Prompt (Midjourney v6):

A surreal conceptual scene of a giant semi-transparent elephant standing inside a small dimly lit bedroom, the elephant is composed of faint glowing numbers and bond certificate patterns, the bed is empty and rumpled, soft blue moonlight through curtains, the elephant occupies most of the room, muted greys and steel blues with faint golden glow, no human figures, no text --ar 16:9 --v 6 - Prompt (DALL-E 3):

16:9 surreal conceptual scene: a giant semi-transparent elephant standing inside a small dimly lit bedroom, the elephant composed of faint glowing numbers and bond certificate patterns, an empty rumpled bed, soft blue moonlight through curtains, the elephant dominates the room, muted greys and steel blues with faint golden glow, no human figures, no text.

Image 2: Yield-Price Seesaw

- Placement: End of yield section

- Emotional Anchor: Counter-intuitive, logical

- Color Tone: Blue-green contrast

- Prompt (Midjourney v6):

Abstract conceptual illustration of a seesaw in a soft studio setting, the left side holds a glowing blue cube with rising arrows, the right side holds a falling golden block, the seesaw is balanced at the apex, clean minimalist style, soft lighting, no text --ar 16:9 --v 6 - Prompt (DALL-E 3):

16:9 abstract conceptual illustration: a wooden seesaw in a soft studio setting, the left side holds a glowing blue cube with rising arrows, the right side holds a falling golden block, balanced at the apex, clean minimalist style, soft lighting, no text.

Image 3: Yield Curve Inversion

- Placement: End of yield curve section

- Emotional Anchor: Warning, comparison

- Color Tone: Warm orange (normal) vs cool red (inverted)

- Prompt (Midjourney v6):

Two side-by-side abstract line charts on a soft grey background, the left chart shows a smoothly rising warm orange curve from left to right, the right chart shows a downward-dipping cool red curve that crosses itself in an X shape, clean data visualization style, no text, no labels --ar 16:9 --v 6 - Prompt (DALL-E 3):

16:9 two side-by-side abstract line charts on a soft grey background, the left shows a smoothly rising warm orange curve from left to right, the right shows a downward-dipping cool red curve that crosses itself in an X shape, clean data visualization style, no text, no labels.

Image 4: Three-Bucket Asset Allocation

- Placement: End of three-bucket section

- Emotional Anchor: Action, clarity

- Color Tone: Green, blue, orange — three roles

- Prompt (Midjourney v6):

Abstract conceptual illustration of three large wooden buckets standing in a row on a clean studio floor, the leftmost bucket is deep green and solid, the middle bucket is calm blue and steady, the rightmost bucket is bright orange and lively, soft top-down studio lighting, warm wood floor, no text --ar 16:9 --v 6 - Prompt (DALL-E 3):

16:9 abstract conceptual illustration: three large wooden buckets standing in a row on a clean studio floor, the leftmost deep green and solid, the middle calm blue and steady, the rightmost bright orange and lively, soft top-down studio lighting, warm wood floor, no text, no labels.

Comments