You think holding a dozen positions diversifies your risk—but you’re actually just sprinkling money into highly overlapping assets. You envy the brute force of concentrated investing, but you overlook the cognition, capital, and resilience behind it that you don’t have.

Investing is never a binary choice—it’s a dynamic balance that matches your stage of life. Pick the wrong weapon, and no amount of effort will help.

Open any ordinary retail investor’s account, and you’ll likely see this: a dozen stocks spanning consumer, tech, finance, pharma, plus all kinds of thematic ETFs. At first glance, assets cover the entire market, risk has been broken into pieces, and the sense of security is at maximum.

But the moment the market wobbles, almost every holding drops in lockstep—none can stand alone. The diversification effect is gone. Even more frustrating, even if one position doubles, its contribution to the whole account is negligible. Your principal has been sliced into countless fragments—no matter how they tumble, they can’t form a snowball big enough to weather the storm.

This is the “fake diversification” trap most people are stuck in.

1. The Century-Long Debate: Diversification vs Concentration—Which Is the Wealth Code?

The investing world has been debating this for over a century: which is the real wealth code?

- One side: the founders of Modern Portfolio Theory, who used mathematical models to prove that low-correlation asset combinations can reduce volatility without sacrificing returns. This theory became the core principle for institutional capital allocation.

- The other side: investment masters who say outright: “Diversification is protection against ignorance.” People who really understand investing focus their energy on a few quality targets and earn excess returns.

The two views seem diametrically opposed, but behind them lies a core truth the masses ignore: there is no absolute right or wrong between diversification and concentration—only whether it’s appropriate.

Discussing strategy without considering your own conditions is like carving a boat to find a sword—you’ll never find it.

Many people’s understanding of diversification stops at the surface: “don’t put all your eggs in one basket.” They’ve never dug into the deeper logic.

The core of diversification was never about the quantity—it was about the low correlation between assets. It’s about having different assets hedge each other during market swings—when one falls, another can hold up, smoothing the overall portfolio’s volatility. Like preparing different vessels for a sea voyage to handle storms, hidden reefs, and currents—ensuring the whole journey stays steady.

The classic application of this logic is the multi-asset approach used by top institutions—abandoning the traditional single stock-bond combo and incorporating alternative assets, using different types of assets to navigate multiple market cycles and achieve long-term stable growth.

The real value of diversification was never maximizing returns—it’s reducing emotional interference so you survive long enough.

Market volatility is the norm; black swan events can happen any time. When a single asset or sector takes a hit, diversification drastically reduces drawdowns and keeps you from panic-selling at the bottom and missing out on compounding. It’s the psychological seatbelt on the investment road, helping you stay rational through the market winter until spring returns.

But this perfect theory keeps failing in retail investors’ hands. The problem isn’t the theory itself—it’s that what they practice was never real diversification. It’s self-deceiving fake diversification.

2. Three Deadly Traps of Fake Diversification

Trap 1: Diluted Returns from Position Overload

The most common rookie mistake is being driven by every piece of news. You see a hot target and want in; someone recommends something and you buy blindly. Before you know it, your account is buried with a dozen or even twenty-something positions.

Your capital is endlessly diluted, each position has a tiny share, and even if you pick winners, the returns get sucked dry by mediocre picks.

Like cutting a cake into dozens of pieces, each one is too small to taste—never sweet enough. The principal that could have rolled into a snowball becomes dust scattered in the wind, never able to form compound interest.

Worse, the more positions you hold, the harder it is to track them. Working people don’t have the energy to study every company’s financials, industry dynamics, and operational changes. Information asymmetry gets worse, you miss stop-loss signals and add-on opportunities, and you end up passively absorbing losses.

Trap 2: Looks Diversified but Highly Overlapping

Many people love buying multiple ETFs with different names, thinking that covers the whole market. But crack open the holdings and you’ll find the core positions are heavily overlapping—essentially the same batch of assets in different packaging.

For example, multiple broad-based and thematic ETFs have highly similar top-10 holdings, with core weighted stocks appearing repeatedly. You think you bought different products, but you’re actually concentrated in the same batch of companies. Risk hasn’t been diversified at all—and you’re paying more in management fees to boot.

Today’s market is increasingly top-heavy, with concentration in leading companies rising. Single-sector leaders take up huge weights in indices. The so-called “whole-market exposure” is largely betting on a handful of companies’ fates. Once an industry cools or policy shifts, the whole account moves sharply.

Trap 3: Paralysis During a Crash

In a bull market, broad gains mask every problem. Investors holding many positions will mistake their luck for skill. But when the bear arrives, all assets fall together, and without adequate cash reserves, you don’t know which one to save or which one to abandon.

A dozen positions all sound the alarm at once—the brain simply can’t process the flood of information fast enough. You either cut blindly or go full flat-on-your-back, watching losses balloon.

Even full-time investors struggle to track dozens of companies at once—working people stand no chance. Diversification becomes a burden, leaving you powerless in a market crisis.

3. Real Diversification Must Meet Two Prerequisites

Real diversification must meet two core prerequisites—either one missing renders it ineffective:

Prerequisite 1: Assets in the Portfolio Must Have Genuine Low Correlation

Stocks, bonds, commodities, alternatives—these have different drivers of returns and can hedge each other. Overlapping same-industry, same-attribute positions just re-expose risk without any diversification benefit.

Prerequisite 2: Principal Scale Must Match Diversification Degree

Excessive diversification with small capital dilutes returns so much that even basic compounding can’t kick in. No matter how perfect the math model, it can’t overcome real capital constraints.

Without these two conditions, “diversification” is just spreading money across different places—risk isn’t reduced, returns get diluted, fees increase, and it becomes the worst possible investment strategy.

4. The Truth About Concentration: Not Gambling, But Precision Betting on Deep Cognition

After seeing the traps of fake diversification, many people turn to concentrated investing, attracted by its brute force, not realizing concentrated investing is an even more dangerous arena.

The core logic of concentrated investing is to focus on a few quality targets, putting capital into businesses you truly understand to earn excess returns. In a winner-takes-most era, leading companies capture the lion’s share of industry profits, with moats in technology, brand, and channels—long-term growth certainty far exceeds smaller players. Concentrated holdings in these companies are how you capture the core opportunity of wealth growth.

But what most people call “concentrated investing” is blindly heavy-loading a single stock—gambling, not true value focus.

Investment masters’ concentrated investing was never gambling—it’s precision positioning built on deep cognition.

They spend months or even years researching a company, fully understanding its business model, management quality, industry landscape, moat, and advantages. Only after confirming long-term value do they go heavily positioned, always staying alert, and adjusting their strategy as the company evolves.

More importantly, they have abundant cash reserves. Even when markets plummet, they can calmly add positions without being knocked off rhythm. Behind this are three core capabilities retail investors can’t replicate:

- Deep research ability

- Exceptional psychological resilience

- Ample capital reserves

The gap between retail investors and professionals has never been about capital—it’s about cognitive depth and risk tolerance. Retail investors mostly rely on secondhand news and short-term trends, lacking understanding of business fundamentals. Professionals can see through the surface to long-term value.

When a stock gets cut in half, retail investors panic, lose sleep, and sell in fear. Professionals calmly assess whether it’s opportunity or risk. More critically, retail investors’ investment capital is often tied up with living expenses, lacking emergency reserves. The moment they need cash, they’re forced to sell at the bottom—even great stocks become losses. Professionals keep investment capital fully separate from living expenses, allowing them to hold long-term across cycles.

Research shows that over the long term, the vast majority of wealth creation in the market comes from a tiny number of quality targets. The rest have mediocre returns—even worse than risk-free rates. Even institutional investors with professional teams and massive resources fail to beat the market at a high rate. How can retail investors, with only fragmented information, precisely pick the few super winners?

Blindly imitating concentrated investing isn’t investing—it’s gambling with hard-earned money, and the most likely outcome is becoming the market’s sacrificial lamb.

5. Human Capital: The Real Asset You Overlook

So how should ordinary investors choose? Stick with the diversification shield, or try the concentration spear?

The answer lies in the human capital you’ve never valued.

For most people, the core asset isn’t the money in your brokerage account—it’s your future decades of work income.

When you’re young, you have less principal but a long working life ahead, so human capital is highly valuable. Even if your investment account takes a hit, you can recover through future earnings—you have the capital for trial and error. As you age, human capital gradually decreases, financial assets become your livelihood safety net, and you must shift to stability, avoiding large volatility risks.

This means your investment strategy isn’t static—it dynamically adjusts with age, principal, career, and mindset.

- Young, small principal, stable career, strong resilience: you can moderately increase offensive allocation, try concentrated positioning, and accumulate experience through trial and error

- Middle-aged, ample principal, heavy family responsibilities, dependent on investment income: must prioritize defense, preserve principal safety, pursue steady returns

Before choosing a strategy, ask yourself three questions:

- Do you have above-market cognition in a specific industry?

- Can you handle the volatility of a heavy position getting cut in half?

- Are your investment capital and living expenses fully separated?

Only when all three answers are “yes” do you qualify to try concentrated investing. Otherwise, diversification is the most rational choice.

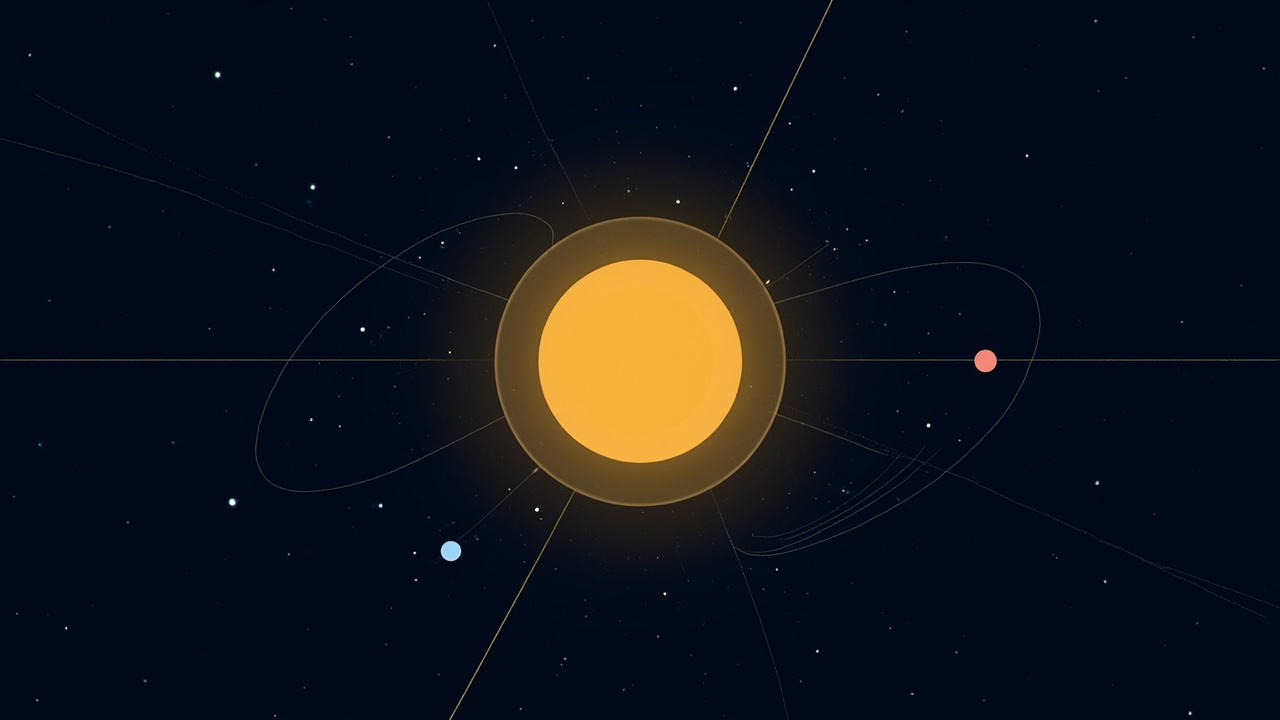

6. The Core-Satellite Strategy: The Optimal Solution for Ordinary Investors

For the vast majority of ordinary investors without professional background, time for research, and seeking stability, the Core-Satellite strategy is the optimal solution balancing safety and returns.

This institutional-grade allocation logic perfectly combines the strengths of diversification and concentration—giving you both the shield’s safety and the spear’s explosive power.

Strategy Logic

The Core-Satellite strategy is simple—divide your portfolio into two parts, like a solar system: a stable sun at the core and flexible planets as satellites.

| Position | Weight | Purpose | Target Selection | Discipline |

|---|---|---|---|---|

| Core | 70-80% | Safety baseline, ballast | Low-cost broad-index funds or total-market ETFs | Hold long-term, don’t move easily |

| Satellite | 20-30% | Return amplifier | Targets you’ve deeply researched and truly understand | Focus on your circle of competence, take controlled risk |

Choosing the Core Position

The core position, weighing 70-80%, serves as the portfolio’s ballast. Choose low-cost broad-index funds or total-market ETFs that track market average returns—diversified across sectors and stocks, effectively avoiding single-target black swan risk.

Just hold long-term and share in the economy’s growth dividend. This is your safety floor—whatever the market does, don’t disturb it easily.

Choosing the Satellite Position

The satellite position, weighing 20-30%, serves as the return amplifier. Allocate to targets you’ve deeply researched and truly understand—familiar industry leaders, long-term-favored thematic tracks, quality alternative assets, etc.

This capital pursues excess returns—even if it loses, it doesn’t threaten the overall portfolio’s safety. But if you get it right, it can dramatically boost overall returns.

The satellite position’s core is focusing on your circle of competence—don’t follow the herd blindly, only invest in what you understand and can track.

Dynamic Adjustment of Ratios

Importantly, the Core-Satellite ratio isn’t fixed—it adjusts dynamically:

- When young: small principal, abundant human capital—you can moderately raise the satellite ratio for more aggression

- As you age: principal accumulates—gradually increase the core ratio, lower the satellite ratio, shift toward stability and defense

- Approaching retirement: core can rise above 85%, satellite compressed to around 10%, maximizing principal safety

The Critical Step of Rebalancing

In strategy execution, rebalancing is a critical step you absolutely cannot ignore.

Over long-term holding, some satellite targets may rise sharply, causing their weight to exceed initial settings. The portfolio shifts from diversification to de facto concentration, and risk rises sharply. Conduct an annual rebalance:

- Sell assets that have risen too much or exceeded their target weight

- Top up the core position or other undervalued satellite assets

- Return the portfolio to its preset ratios

This counter-intuitive “sell the strong, buy the weak” move is the core discipline of diversification—it helps you lock in gains and buy low. Persist long-term, and returns far exceed blind holding.

7. The Essence of Investing: Monetizing Your Cognition

The essence of investing is monetizing your cognition—matching it to your own conditions.

Many investors don’t fail because the market is too cruel. They fail because they’re using the wrong weapon for the wrong battle—

- Young people clinging to shields, missing growth opportunities

- Elderly people gripping spears, recklessly aggressive, endangering their later years

This is investing’s greatest tragedy.

Diversification, concentration—there’s no absolute right or wrong, only whether it’s appropriate for the current you.

- Diversification is the shield that protects the ignorant, letting ordinary people keep pace with the market

- Concentration is the spear that monetizes cognition, letting professionals earn excess returns

- The Core-Satellite strategy is the wise choice for ordinary people to balance safety and returns, letting you seize opportunities within stability, find breakthroughs within defense

Don’t get caught up in the diversification-vs-concentration debate anymore. Don’t blindly imitate others’ strategies.

Calmly assess your age, principal, career, and mindset. Find your own investment rhythm. Match the weapon that suits you best.

Investing isn’t about who makes money fastest—it’s about who walks the steadiest and farthest. Hold onto rationality, stick to discipline, match yourself—and only then can you survive long-term in the market and ultimately harvest the fruits of compounding.

Investing has never been about choosing spear or shield. It’s about using the right weapon at the right time, being the right version of yourself.

This article shares personal opinions only and does not constitute any investment advice. All investing carries risk, and past performance does not guarantee future results. Please assess your own risk tolerance carefully and consult a professional financial advisor before making any decisions.

Comments