Let’s start with a brutally honest choice.

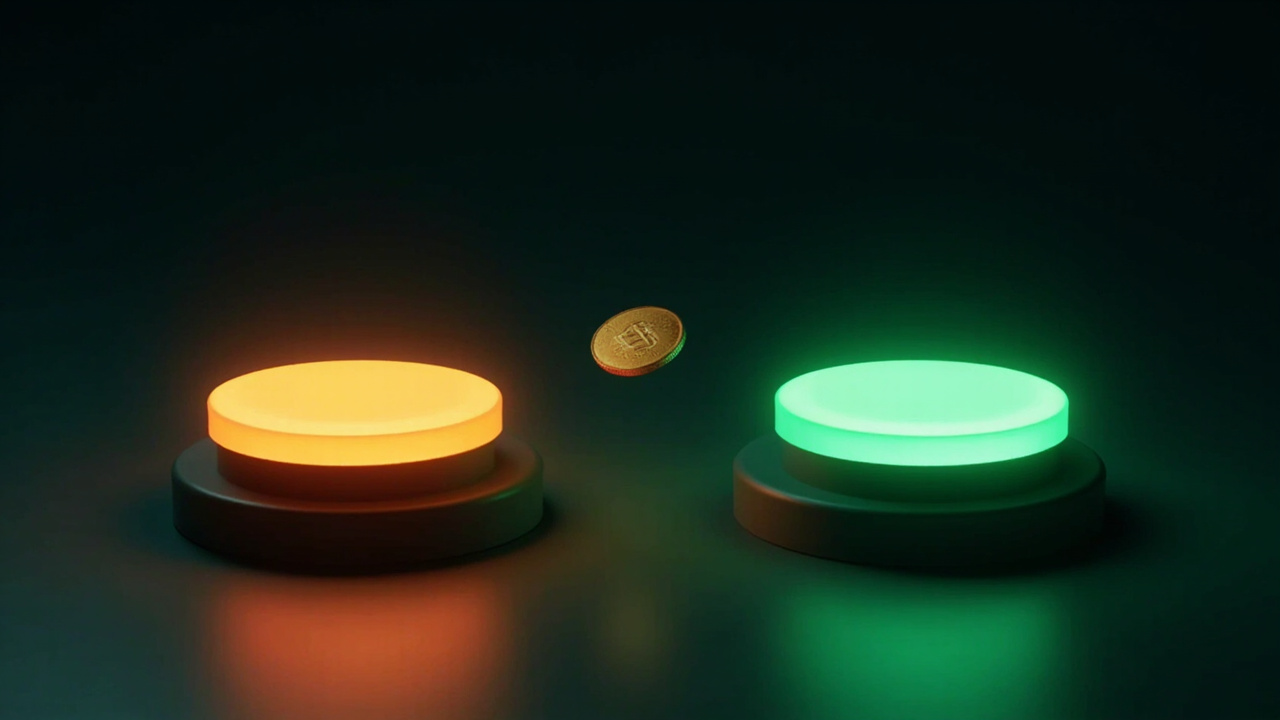

Imagine two buttons in front of you:

- Red button: Press it and receive NT$1 million in cash, deposited instantly into your account

- Green button: Press it and you have a 50% chance of winning NT$100 million, but also a 50% chance of getting nothing

Which would you press?

Don’t answer too quickly. Here’s the truth: the vast majority would choose red—that sweet, safe million in hand, right?

But do you know how people who actually keep and grow wealth think? They’re not braver—they’ve done the math: the expected value of the green button dwarfs NT$1 million. They’d figure out how to break that button into pieces, package it, and sell it to people who can absorb the risk.

This is the first secret I want to share: the dividing line between rich and poor has never been how much money is in your pocket today—it’s what price tag you put on pain and uncertainty.

If you can’t tolerate the momentary pain of possibly getting nothing, you’ll only ever claim that NT$1 million. If you’re willing to coexist with uncertainty, you might just touch that NT$100 million.

Today I’m not going to talk about the 36 money-saving tricks or the 72 variations of dollar-cost averaging. I’m going to share something more foundational and more brutal. Once you understand it, you’ll realize that those people earning less than you but somehow buying homes, or those who seem to effortlessly build their first nest egg—they’re not better at enduring hardship than you; they’re better at understanding one term: pain pricing.

1. You’re Not Spending Money—You’re Buying Emotional Band-Aids

Ready to retrain your brain on money? Let’s dissect one of the most everyday, most lethal behaviors: spending.

Have you ever had this experience? You grind until late at night, get bullied by the client 800 times, revise the proposal a dozen times, and finally the client says “let’s just go with the first version.” You shut your laptop feeling completely drained. At that moment, almost involuntarily, you open a shopping app and order some little thing you don’t really need but have been eyeing for days.

Maybe a retro Bluetooth speaker, maybe a pen rumored to give you god-tier handwriting, maybe an outrageously expensive skincare set. When the package arrives and you tear it open, you feel a rush. That rush is like ice-cold cola on a scorching day, like finally exhaling after holding your breath forever.

You call this “treating yourself.” But here’s the brutal truth: this isn’t self-reward. You’re buying yourself an emotional Band-Aid.

You spend money, but what you’re really purchasing is a cheap tranquilizer called “calm.” Your brain is both too smart and too lazy. It discovered a quick fix for pain: spending money.

Got yelled at at work? Spend. Felt compared and found wanting? Spend. Lonely? Spend. Each time you spend, your brain gets a small dopamine hit that briefly covers up the discomfort. But here’s the problem—this Band-Aid doesn’t cure anything. It just covers the wound. And its effectiveness diminishes over time.

The first time, a NT$300 purchase makes you happy for three days. The second time, you need a NT$3,000 item to feel good for one day. Eventually, a NT$30,000 splurge only buys you an afternoon of joy.

This is why, even as you earn more, you can’t hold onto your savings. Because you’re not exchanging money for things—you’re exchanging money for emotional medication—and the emotional illness you carry cannot be cured by shopping.

2. Tactical Stinginess, Strategic Waste

Someone might say: okay then, I’ll quit. I’ll stop buying. I’ll save. I’ll pinch pennies. I’ll turn myself into a miser—is that fine?

Sorry, but if all you know how to do is save, you’ll most likely become a poor rich person—or what I’d call an exhausted bookkeeper living a tired life.

I’ve seen too many people like this. They’ll spend 20 minutes across three apps comparing delivery fees to save NT$20, muttering “every bit counts.” They’ll stay up until 2 a.m. on Singles’ Day calculating discount rules with more intensity than high school math, only to stockpile enough paper towels and detergent to last a year, turning their balcony into a mini warehouse.

In summer, they won’t turn on the air conditioner and break out in heat rash. In winter, they won’t turn on the heater and shiver under blankets. They’ll haggle over NT$5 at the market until both parties are red-faced.

And then? The money they so painstakingly saved might disappear overnight because of a friend’s bad investment tip. More commonly, on some emotionally-broken late night, they go on a revenge-spending spree—blowing half a month’s salary on an unnecessary feast, or buying some outfit that still has the tag on it in the closet.

This kind of saving isn’t financial planning. It’s tactical stinginess paired with strategic waste.

Why? Because you’ve sold your most valuable asset—your time and attention—at rock-bottom prices. Those 20 minutes you spent price-comparing and coupon-clipping, if instead spent learning a new skill or figuring out how to be more productive at work, could yield long-term returns thousands of times that NT$20.

Real pros save strategically—and they waste strategically too.

I have a story of my own. When I first started working, my income was low, but I would religiously set aside 15% of it each month for something that made everyone around me think I was crazy: going to the most expensive coffee shop in the city, staying at a five-star hotel I couldn’t afford, or attending ridiculously expensive industry talks.

My colleagues said I was pretending, said I was punching above my weight. But only I knew what I was doing.

In that ridiculously expensive coffee shop, I overheard the next table discussing Series A funding rounds and business models. I jotted those terms down, researched them for a month, and by the time I interviewed for my next job, I could speak fluently about industry trends.

In the executive lounge of that five-star hotel, I watched how truly wealthy people talk, dress, and interact—my taste, my conversational skills, my worldview quietly upgraded through that one piece of “strategic waste.”

What was I buying? Information asymmetry and a ticket into the inner circle.

This is the highest level of saving: pull the money from your spending account and dump it—hard—into your leverage account.

What is leverage?

- Knowledge is leverage: it makes one hour of your work worth ten hours of someone else’s

- Networks are leverage: they reveal opportunities others never see

- Health is leverage: it lets you work ten more years and enjoy ten more years of compounding

- Aesthetics are leverage: with equal ability, well-presented people get far more opportunities

So stop agonizing over that NT$20 delivery fee. If you spent that half hour figuring out “how can I negotiate NT$20,000 more in my next raise,” your world would look entirely different.

Spend money on things that make you more valuable, not things that make you look more expensive. The former is investment; the latter is consumption—one letter’s difference, worlds apart.

3. Before You Buy Any Stock, Invest in Your Pain Tolerance

Mindset is set, money is saved—so what’s next? Investing—buy funds, stocks, ETFs, let your money make money. Sounds right? Yes, but not deep enough.

I want to share a perspective that might flip your worldview: before you buy a single stock or fund, the first investment you should make—and the most brutal one—is in your own pain tolerance.

What is pain tolerance? It’s your ability to calmly endure how much discomfort, uncertainty, and embarrassment.

Let me illustrate. Have you ever bought a fund? Have you experienced this scene: you confidently buy a hot fund; day two it drops 1%—you say, “no worries, normal fluctuation”; day three it drops another 2%—you start getting nervous; day four it drops 3% more—you completely break down, can’t sleep, brain screaming “I’m done, my hard-earned money is gone.” On day five, you can’t take it anymore and sell at a loss—then day six it goes up 5%.

Do you feel like the market is targeting you personally? Like you’re the legendary reverse indicator? The market isn’t targeting you—your pain tolerance is just too low.

You can only handle 1% swings. Once volatility exceeds your threshold, your brain sounds the alarm and forces you to flee. Investing, fundamentally, is a pricing game around volatility. The people who ultimately make money aren’t smarter than you—they can stomach swings you can’t. While you’re scared out of your wits, they calmly add to their positions.

This pain tolerance shows up everywhere in life, not just in investing:

- You don’t dare ask your boss for a raise because you can’t handle the awkwardness and embarrassment of rejection. So you keep tolerating a salary that doesn’t satisfy you.

- You don’t dare quit that miserable job to try what you really love because you can’t bear the insecurity of no stable income. So every Sunday night you’re crushed by the Monday dread.

- You don’t dare speak up in public because you can’t face the risk of being mocked. So your ideas stay ideas, your talents known only to you.

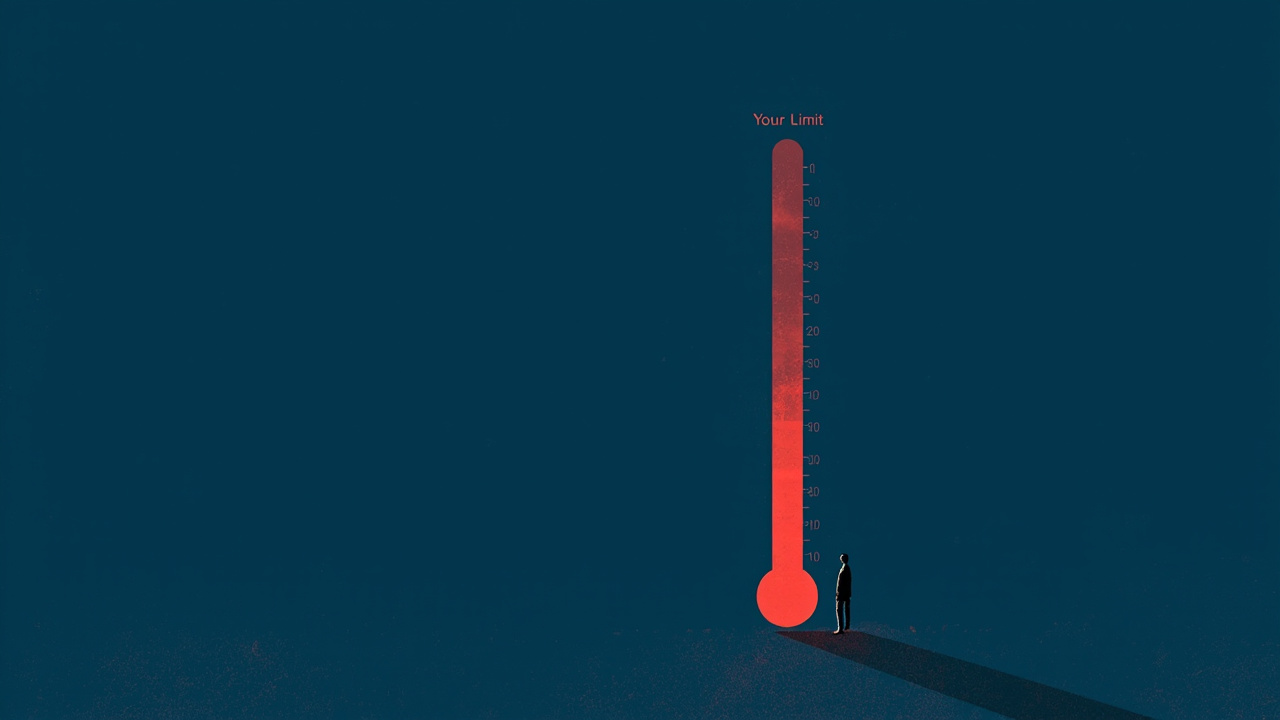

Where is your ceiling? Right on the scale of your pain tolerance. If your tolerance is only 50 degrees, the moment life hits 51 you collapse, break down, retreat to your safe zone. And wealth is never found in the safe zone.

4. Two Wildcard Methods to Build Pain Tolerance

So how do you raise this pain tolerance? Here are two methods I’ve personally tested that work.

Method 1: Voluntarily Seek Small Bitterness—Train Your “Embarrassment Muscle”

Scared of talking to strangers? Fine, then go to the wet market and chat with every vendor, even just to ask “is this fresh today?”

Scared of rejection? Find ten people and ask them a question you know they’ll refuse—“can you lend me NT$1,000?” Each rejection, tell yourself “see, that’s all it was—I didn’t lose any meat.” After 100 rejections, you’ll find your embarrassment muscle is as thick as iron.

After that, asking for a raise? Easy. Confessing to someone you like? Bring it on.

Face—when you stop caring about it, you become invincible.

Method 2: Build Your Mental Bulletproof Vest

Why do poor people often make seemingly stupid short-term decisions—taking out predatory loans, selling important things for a few hundred dollars? Because their lives have no redundancy. They’re like tightrope walkers with no safety net—a small gust can knock them down.

So build your emergency fund. This isn’t just money—it’s your psychological bulletproof vest.

When you have three months of living expenses sitting in your account, your mindset shifts:

- Your boss yells at you and you talk back—because you know you won’t starve

- You see an opportunity that takes long-term investment but promises rich returns, and you dare try it—because you know you can afford to fail

It’s these three months of living expenses that lift your pain tolerance from “I’ll starve tomorrow” to “I won’t panic even without work for three months.” That upgrade makes every decision you make calmer, more rational, more far-sighted.

5. Ten Years Isn’t a Red Line—It’s the Track You Lay

Finally, let’s talk about ten years. Thinking on a ten-year timescale is great, but I want to add a critical caveat: never rely on willpower to last ten years.

Willpower is a consumable, like a phone battery that goes red after heavy use. People who persist at something for ten years aren’t stronger-willed than you—they’ve designed a system that pushes them forward, so they don’t need much willpower at all.

Let me break it down for you:

System Design 1: Environmental Design

Is your phone full of shopping apps? Are your subscriptions full of content telling you what to buy? Do the influencers you follow just flaunt cars and trips all day? You’re soaking yourself in a chamber of consumer poison. If you don’t bleed, who will?

You need to actively detox: turn off all notifications from those shopping apps, even hide them in the last folder on your phone to add friction; unfollow influencers who make you anxious and trigger comparison; follow people who share genuinely useful content—business logic, self-management, long-term investing.

System Design 2: Social Environment

Do you have friends whose every conversation is “where did you go, what did you buy, which restaurant is good”? That’s a classic status-show circle. Consciously move toward people who play the asset game—those who discuss this month’s passive income, what they’re reading lately, how to improve work efficiency.

It’s not about becoming mercenary—environments shape people drop by drop. As the saying goes, you are the average of the five people you spend the most time with. Look at your five—who’s helping you accumulate assets, who’s helping you burn them?

System Design 3: Feedback System

Why are games so addictive? Because they give instant feedback—you slash a monster, blood splashes, damage numbers pop up, the experience bar inches forward.

Saving and investing have painfully long feedback loops. You struggle for a month, your account grows by NT$3,000, you feel nothing—dry, hard to stick with.

Then design your own feedback. Turn your savings goal into a vivid image. Want to save up to see the Northern Lights in Iceland? Print out photos of the aurora and stick them on your fridge, your bedside, your desk. Every time you save NT$10,000, drop a glass marble representing NT$1,000 into a “Iceland Fund” jar.

When the marbles keep piling up—your hand can feel them, your eyes can see them filling the jar—the feeling is completely different. You don’t need to force yourself. You’re being pulled forward by desire.

Ten years isn’t a red line you have to leap over with willpower. It’s a gentle slope you glide over using systems, environments, desires, and habits. Just lay the track at the start; let time do the rest.

6. A Letter of Challenge to You

We’ve covered a lot—emotional spending, strategic waste, pain tolerance, life system design. I know your head is spinning, you might be thinking “this is too hard, too much to change.”

But here’s what I want you to know: you don’t have to do it all. Pick one or two that resonate most and start.

But here’s an extra caveat: don’t pick the easiest one or two—pick the one or two that make you most uncomfortable. Because the spot that makes you most uncomfortable is exactly where your pain tolerance is lowest—and that’s the biggest chink in your life’s armor.

- Most afraid to talk about money with people? This week, find someone and ask them to pay back the few hundred dollars you lent them. Not for the money—to practice tolerating the pain of confrontation.

- Most afraid to face your bills? Tonight, export every spending record from every app, line by line, and read through it—even if it makes your heart race. That’s practicing tolerance for truth.

- Most afraid of boredom? Right now, put your phone aside, turn off every screen, and sit in silence for 15 minutes doing nothing—feel the boredom crawling over you like little insects. That’s practicing tolerance for the prelude to deep work.

Finally, I want to say one thing to you:

Ten years from now, you won’t thank the “you” who merely listened to this article—listening is too easy, painless, itchless. Ten years from now, you’ll only thank the “you” who took action—the one who, even afraid, even in pain, even uncertain, even thinking this was too hard, still gritted their teeth and took that one small step.

This article isn’t a guide. It’s a declaration of challenge. I’m issuing it to you—do you dare accept?

From today, from this second:

- Refuse to keep playing the status-show game others designed

- Walk away from the rat-race competition that’s draining you

- Start playing your own game

This game is called “Life Upgrade.” The rule is just one: continuously, deliberately, gently, but firmly, raise your own pain tolerance.

- When you stop fearing embarrassment, you gain courage

- When you stop fearing uncertainty, you gain wisdom

- When you stop fearing boredom, you gain focus

Once you have courage, wisdom, and focus—do you think money will still be a problem?

Don’t be anxious, don’t compare. From now on, only compete with yesterday’s self—tolerating a little more pain each day. Ten years from now, we don’t need some cheesy reunion at the peak.

Ten years from now, when you have the confidence to walk away from anyone you don’t like, from any place you don’t like; when you have the calm, steady power to say “no” to toxic people and toxic things; when you’ve become the version of yourself you most wanted to be—that moment is your life’s peak.

Now close this article and go do that small uncomfortable thing. Right now. Immediately. See you at our respective peaks ten years from now.

This article reflects personal opinions only and does not constitute investment advice or therapy. Please evaluate your own situation carefully when making investment or spending decisions and consult a qualified financial advisor or therapist if necessary.

Comments